In light of the nearly 9% drop in the S&P, the Stableford Capital preservation investment strategies portfolio positioning highlights the difference between active and passive management. We have made moves over the last few weeks lowering portfolio volatility and increasing cash with lower duration and higher yield in mind. We currently have plenty of cash and fixed income so we are well positioned for this move. Within the equity portfolio we have stayed with high quality names and very little small cap exposure (small caps have been hit the hardest). We remain comfortable with the positioning as a whole.

Is it Over?

We keep getting asked if the stock market correction is over and that answer is that it ends only once we stop being asked the question. Even if you do not believe this is morphing into an outright bear market, this isn’t even yet an average plain-vanilla correction despite all the angst. Angst isn’t panic, and the bottoms are turned in only when the panic sets in.

“I would love to see the individual investors more fearful right now,” said Liz Ann Sonders, Chief Investment Strategist of Charles Schwab . “It doesn’t quite feel yet that we’re at the kind of washout point. This probably has more to go.”

And yet individual investors are optimistic? According to an article in Bloomberg, for a third week in a row, individual investors bought stocks while institutional and hedge funds were net sellers (data on client flows compiled by Bank of America). When it comes to stock investing, the gap between main street and wall street is widening.

Stay Vigilant to Risk Adjusted Returns

Everybody is saying “what happened that caused such a meltdown?” Investors search for answers, and the reality is that when it comes to financial markets, there isn’t always a rhyme or reason. People should recognize that volatility is part and parcel of the landscape and that markets move in both directions.

What goes around, comes around.

This is why we insist that Stableford portfolio managers work so closely with advisory services, especially during times of volatility. Our ability to cut exposure and respond to the markets quickly by applying our proprietary risk management process is a testament to the promise we have made to our clients – to actively ensure their investments are aligned with their values, financial goals and the changes in the market.

Take a Breath in Capital Preservation Investment Strategies

Even though it feels like we never leave the trading desk, I’d be remiss not touching on October’s action—the sharpest decrease in the Dow since March. Corporate earnings results from the major banks have been the canary in the coal mine – net operating income was overshadowed by the continued decrease in credit.

Until it becomes clear that a market bottom is in, and for us that means that most everything gets closer to being washed out from sentiment to valuations to market breadth, we will trade greed for patience.

The fact that we still have 45% of the S&P 500 trading above their 200-day moving average doesn’t really scream ‘capitulation’ for Stableford strategies when the norm is 28% at correction lows. In terms of valuations, while they have improved – a 15.7x forward P/E Ratio multiple is still more than 1 point above the 14.5x norm (mean reversion alone will take the S&P 500 to 2,530 or 200 points away from where we closed towards the end of October).

How is Stableford Positioned?

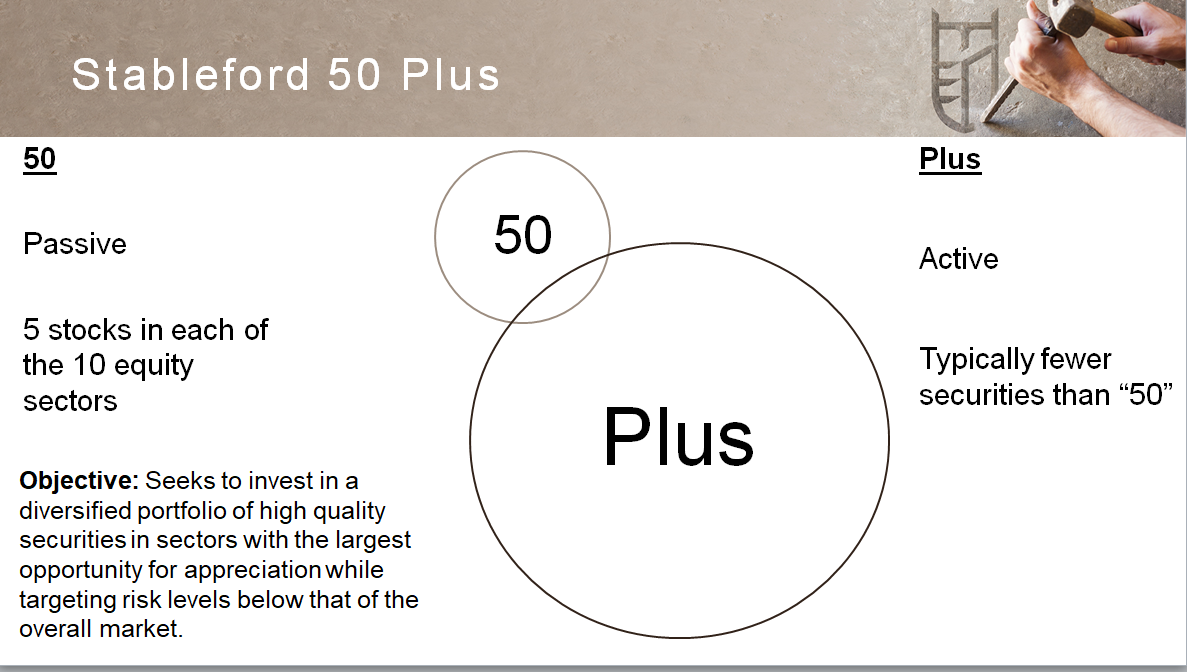

In the Stableford 50 Plus, the largest of our strategies, we have been fairly defensive for a while. We began October at roughly 40% fixed income and cash. And of that number, nearly 30% is in cash or cash-like (variable rate bonds). We reduced our long duration fixed income (riskiest during rate increases – because principal value falls as rates increase) in October, prior to the rate spike.

In the Stableford 50 Plus, the largest of our strategies, we have been fairly defensive for a while. We began October at roughly 40% fixed income and cash. And of that number, nearly 30% is in cash or cash-like (variable rate bonds). We reduced our long duration fixed income (riskiest during rate increases – because principal value falls as rates increase) in October, prior to the rate spike.

On the equity side we are comfortable with the names we hold. By and large, these are higher quality companies with competitive advantages and relatively stable businesses. They can still be volatile, like the market, but over the long term should do well.

Overall, the Stableford 50 Plus moves at 57% of the market. For example, if the market goes down 1%, our portfolio falls 0.57%. The reverse is true if the market moves up.

We have made some changes in October, such as cutting back our exposure to banks and adding some more value-oriented positions as a part of our overall capital preservation investment strategies.

Why Not More Defense?

With the Stableford 50 Plus at less than 52% equity market exposure and the market getting less expensive based on 2019, there is risk of getting too bearish and missing out to the upside. Currently the S&P 500 trades at ~ 15x 2019 EPS, roughly in line with historical averages. Certainly, it could go lower, but it is hard to see it a lot lower given the U.S. economy is still growing nicely. If earnings remained the same and the multiple dropped to 14x (6.7% lower), the market would start to look somewhat cheap, all else being equal.

In addition, many of the signs that usually accompany deep fundamental problems have been absent thus far:

- The overall economy is doing well

- Credit spreads (sign of risk) have widened, but not to levels that indicate deeper problems like in 2009, or even early 2016

- Little evidence of wildly mispriced assets (like home prices in 2009)

- Investors don’t appear to be flocking to “safe harbors” such as gold

- Currency markets have not shown much panic

- Trading for the most part had been orderly, if volatile, in most markets

While markets are volatile, there doesn’t appear to be a deep fundamental problem that would justify a large, and sustained, equity correction.

The Advantage of Active Portfolio Management

As we have witnessed from the recent market fluctuations, active management continues to play a key role in helping to preserve wealth.

Said simply, if you 50% of your hundred dollars, it takes 100% return to get you to break even.

Active capital preservation investment strategies to Stableford Capital means the constant attention to the portfolio construction process – not to be confused with trading. It means that to have risk-adjusted returns you need to have a tactical allocation to your portfolio. The road to compounding money is still hidden in the volatility of the returns.

Investment advisors that employ a consultative, integrative approach, like Stableford keep you in step with the market. As a client, find out how your interests are placed at the forefront of every investment decision, call us at 480.493.2300 or contact us here.