Stableford Capital—January 2021 Review: On Bubbles and Government

“One of the hallmarks of every bubble is a loss of interest or ability of investors to distinguish between investment and speculation. Once that mentality has taken hold, and prices become wildly elevated, it is impossible to sustain the bubble without also making its consequences worse.” – John Hussman, Ph.D.

Equity markets are getting frothy, no doubt about it. We are starting to see behavior that is untethered from reality. Blank check SPACs as far as the eye can see and Robinhood investors pumping up stocks from their iPhone apps—without regard for valuation—are but a few of the signs.

But that doesn’t mean that everything will come crashing down soon. This is what makes irrational behavior so difficult—just because it has been identified doesn’t mean it will stop.

In fact, those that are charged with preserving our economic wellbeing are most intent on keeping the music playing, without regard to the negative consequences. Witness Fed Chairman Powell’s comments last month, “…I think that the connection between low interest rates and asset values is probably something that’s not as tight as people think…” OK, we know he is trying to keep the economy going during a pandemic and all, but let’s be clear as to the source of the asset inflation: Artificially low interest rates and Fed liquidity. It’s not like we haven’t seen this movie before.

Recall then-Chair Yellen in 2005 commenting on asset bubbles, not long before the housing bubble popped:

“How then, should monetary policy react to unusually high prices of houses – or of other assets for that matter? In my view, it makes sense to organize one’s thinking around three consecutive questions – three hurdles to jump before pulling the monetary policy trigger. First, if the bubble were to deflate on its own, would the effect on the economy be exceedingly large? Second, is it unlikely that the Fed could mitigate the consequences? Third, is monetary policy the best tool to use to deflate a house-price bubble? My answers to these questions in the shortest possible form are, ‘no,’ ‘no,’ and ‘no.’”

Fear not! Dr. Yellen was recently sworn in as Treasury Secretary. So, between the uber-dovish Fed and trillions of dollars of government stimulus from the new administration, this behavior can persist for a long time.

But while we don’t know when the music stops, we do know what happens. And it won’t be pretty. Of course, that’s where Stableford comes in. We are aware of these factors. Our goal is not to be tied to one viewpoint, be it perma-bear or perma-bull, but to take measure of all views and set a prudent course. At this point, we’re becoming more cautious. There is some irrational behavior in the marketplace, and bubbles are likely being formed. It doesn’t mean that we need to get wildly bearish, but we are definitely becoming more cautious.

January Equities

After an initial runup, the equity market finished January in lackluster fashion, down 1.1%. The drop at the end of the month was driven by margin calls, as regulators required more collateral given the high levels of volatility—driven by traders bidding up high short interest and penny stocks. Who needs Vegas when the casino is on your phone!

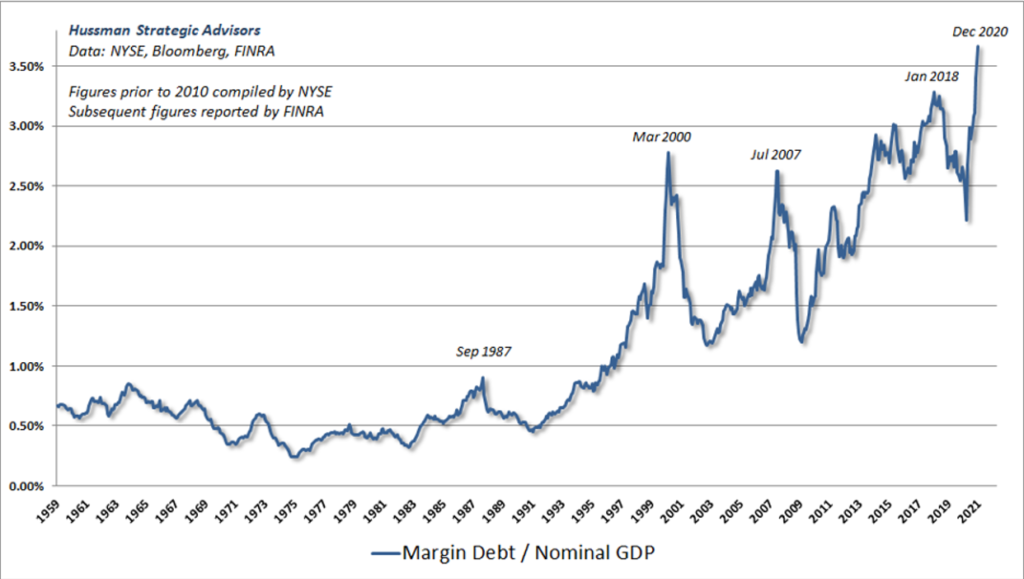

This leads us to another point. Margin debt to Nominal GDP is at an all-time high, making the risk of the next real pullback more precipitous. The dates of the previous peaks for this measure below in Figure 2 may ring a bell, particularly the excesses of 2000. Any negative catalyst is likely to have a large impact given these high levels of margin debt.

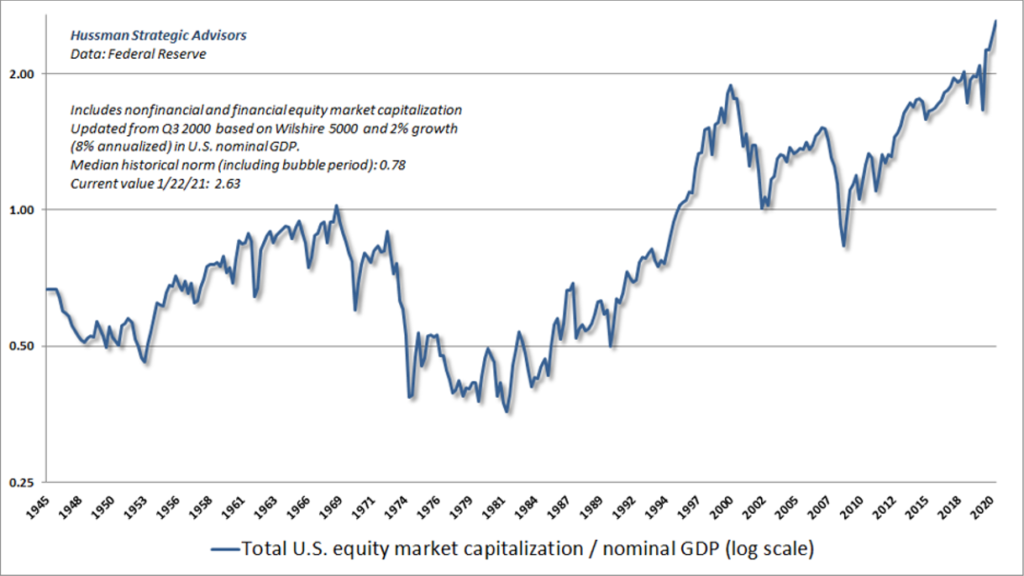

Similarly, equity market valuations at extended, leaving little room for value buyers to step in (Figure 3).

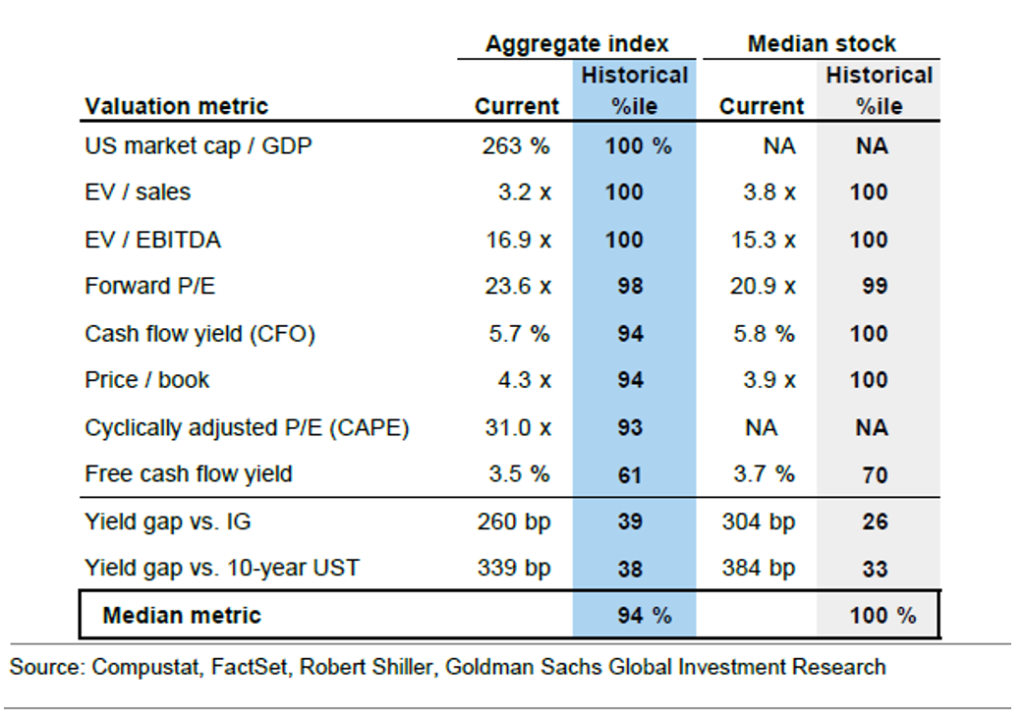

Figure 4 shows similarly high equity valuation metrics, near the top of historical measures on almost every measure. The two metrics that are not near highs, the Yield Gaps, are dependent on interest rates. Interest rates are artificially low right now, driven by Fed purchases. This is a key debate: Are equities less expensive than they seem because they are cheap vs interest rates; or are they expensive due to Fed intervention? Time will tell, but it doesn’t bode well for the day the Fed reduces bond purchases.

Fixed Income

Regardless of what the Fed desires, interest rates continued their climb in January, with 10 Yr. US Treasury rates rising 16 basis points to close at 1.07%. As we’ve previously mentioned, equities can continue to climb in the face of modestly increasing rates. However, if rates were to accelerate rapidly, it would be problematic for equity appreciation.

In summary, it is clear the government is hell-bent on keeping the money spigots open without regard for potential negative consequences. We are starting to see some of the irrational behavior associated with those consequences. Can this behavior persist? Yes, but prudence dictates that it is time to be somewhat cautious, even if it means leaving some of the upside off the table.

Be Well!

Are you interested in making portfolio changes or getting a more in-depth analysis? Contact Stableford today by calling 480.493.2300 or simply request a copy of our Market Blast.

This market commentary was written and produced by Stableford Capital, LLC. Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested in directly. The views stated in this letter are not necessarily the opinion of any other named entity and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

S&P 500 INDEX: The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.