According to An Inc., 27 million working-age Americans–nearly 14 percent–are starting or running new businesses. (Study data is from a Global Entrepreneurship Monitor (GEM) report initiated by Babson College and the London Business School).

While working for yourself is rewarding and can be quite lucrative, it also presents a unique set of challenges for financial planning. Entrepreneurs, business owners, and independent contractors who have come from the corporate world may find the transition especially bumpy when there is no employer-sponsored retirement plan or even a consistent paycheck (at least in the beginning).

Honing a few key financial planning strategies for the self-employed will help make those hard-earned paychecks go as far as possible and work in your favor.

Financial Planning for Self-Employed Retirement

All too often, people who start a business or transition to working for themselves focus on the work while getting lost in the administrative side of things. Whereas an HR department once handled your retirement account (and maybe even matched funds), now it falls on you to set up your own account.

All too often, people who start a business or transition to working for themselves focus on the work while getting lost in the administrative side of things. Whereas an HR department once handled your retirement account (and maybe even matched funds), now it falls on you to set up your own account.

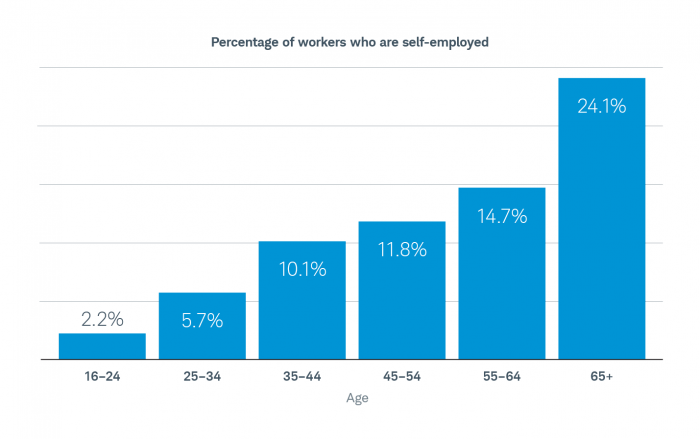

But it’s important – just as important as business development and managing client relationships. The U.S. Bureau of Labor Statistics reports that self-employment rates rise with age, and 14-24% of self-employed individuals are close to retirement age. Then what will you do when you can’t or don’t want to work anymore?

One of the easiest financial planning strategies for the self-employed is to simply start saving. Yet discerning which type of account is right for you can depend on many factors. If you have a 401(k) from a previous employer, you can leave it, roll it over or cash it out (not usually recommended).

One of the easiest financial planning strategies for the self-employed is to simply start saving. Yet discerning which type of account is right for you can depend on many factors. If you have a 401(k) from a previous employer, you can leave it, roll it over or cash it out (not usually recommended).

Rolling over to an IRA, in particular, may benefit the self-employed because it offers more investment choices, lower fees, fewer rules and estate planning perks.

If you are starting fresh or adding a retirement account, you have five main options:

1. Traditional or Roth IRA

Ideal if you are just getting started, and/or have less than the $6,000/year max to contribute ($7,000 for age 50+). You can possibly then deduct contributions made to a traditional IRA from your taxes or plan to take your Roth IRA withdrawals tax-free.

2. Solo/Individual 401(k)

Ideal for an entrepreneur with more to contribute and no employees. You are treated as both the employee AND employer in this account. As the employee, you can contribute up to 100% of your salary or earned income and as the employer, you can contribute an additional 25%. The total 2020 limits here are $57,000 or 100% of earned income – whichever is less ($63,500 for age 50+).

![]()

3. Simplified Employee Pension (SEP) IRA

Very similar to the Solo 401(k) in contribution limits, with less paperwork. However, if you have employees, you must contribute the same percentage of pay to everyone – including yourself.

4. SIMPLE IRA

Ideal for businesses with less than 100 employees, as employees can opt-in and contribute through salary deferral. But you as the employer are required to match employee-made contributions, dollar-for-dollar, up to 3% of their compensation. Contribution limits are $13,500 in 2020 and the matching employer contributions are tax-deductible as a business expense.

5. Personal Defined Benefit Plan

Ideal if you have no employees and want to consistently save a high amount, or amp up your savings before retirement. Much like an individual pension plan, this sets up a defined and guaranteed income into retirement. Your contribution limit is individually calculated based on your age, expected investment returns and distributions at retirement. Note that this individual attention also comes with added administrative fees, plus higher setup and annual fees.

While there are a myriad of online options to set up most of these accounts (more limited options with the Personal Defined Benefit Plan), the differentiators can come down to the fine print, and there may be drawbacks that you don’t see until you take your first distribution.

It is important to discuss your self-employed retirement options with a financial advisor to determine which is right for you and your financial planning goals.

A Funded Future

With a retirement account in place, the best time to fund it is now. Early funding not only means you’ll have more when you need it, but it sets a precedent for making saving important. There are two strategies when it comes to retirement savings:

1. Set a saving schedule. It doesn’t have to be a lot at first, but getting in the habit of regularly contributing to a retirement account means you are at least contributing something. Treat it as a regular monthly expense and set automatic payments or transfers. As your business takes off, you can always increase the contribution amount to meet the annual max for the account.

1. Set a saving schedule. It doesn’t have to be a lot at first, but getting in the habit of regularly contributing to a retirement account means you are at least contributing something. Treat it as a regular monthly expense and set automatic payments or transfers. As your business takes off, you can always increase the contribution amount to meet the annual max for the account.

2. Apply windfalls. Any extra income can always be applied to your retirement savings in addition to the set schedule. A windfall could be a tax refund, a bonus or a big contract, for instance. This is a good strategy when your income varies from month to month.

Your Financial Planning Insurance Policy

Insurance is another administrative task that may not seem as important as the work you are doing. But consider these questions:

What happens if you can’t work? Or if you (or an employee) makes a mistake on the job?

If you are self-employed, there are several different insurance policies to look into. First and foremost, health insurance. One illness or accident could sweep your savings. Several individual and family plans are available through brokers, directly from insurance companies or the health insurance marketplace.

Secondly, consider disability insurance, especially if your business depends on manual labor that puts you at risk for injuries, or if an injury could keep you from working.

General liability insurance should also be on the table to protect you and your business from a range of claims, including property damage, personal injury and bodily injury. If you own commercial property you can bundle policies together to create a Business Owner’s policy.

Yes, the policy premiums can seem daunting, but keep in mind that both business and health insurance premiums are deductible when you are self-employed. Then add up the potential cost if you don’t have them in place and tragedy strikes.

Pay for Professional Support

In the beginning, it may be all about you – you do all the work for your own business, from seeking out leads to invoicing, and everything in between. Hiring employees is not an option, so you may think the cost of working with professional consultants, like an insurance broker or financial advisor, is too high.

However, this specialized professional support could end up saving you time and money. Instead of researching all the insurance products and retirement accounts available, these professionals will do it for you and help you make the best decision for your specific situation. This is especially true when thinking about the tax nuances for financial planning strategies for the self-employed.

At Stableford Capital, we take an integrated advisory approach and look at your entire financial situation when mapping out your financial plan. This includes the fluctuating income and retirement needs of an entrepreneur, and how the tax code changes affect business owners.

To learn more about how Stableford can take the stress out of financial planning strategies for the self-employed, business owner or entrepreneur, contact us online or call 480.493.2300.