From novice investors trying to balance bills with income, to ultra-high net worth investors looking to protect their legacy, nearly everyone is striving for the same goal: financial wellness. Simply stated, this means having control over your finances to the extent that money does not  drive every decision you make. If you’re well on your way to meeting your financial goals, you can take bumps in the market, and you enjoy the freedom of making choices that help you enjoy life.

drive every decision you make. If you’re well on your way to meeting your financial goals, you can take bumps in the market, and you enjoy the freedom of making choices that help you enjoy life.

But how you get there differs from investor to investor and relies heavily on the psychology of investing.

Money habits start early in life and can be difficult to change. Behavioral finance guides this change in the psychology of investing, and financial advisors who are already fiduciaries are best positioned to coach investors to achieve financial wellness.

What is Behavioral Finance?

Behavioral finance is a subset of behavioral economics, as coined by Nobel Prize winner Richard Thaler. It refers to the psychological of investing: influences and inherent biases that affect how investors make and execute their financial decisions. And it starts with the key principle: communication.

Behavioral finance emphasizes people over product. Open communication between advisor and investor allows the advisor to build a clear picture of the investor’s mindset regarding money.

As an investor, expect thoughtful questions as the advisor gets to know you and observers your visceral reaction to the financial topics. Do you light up when talking about passing your business on to your children? Do you clam up when alluding to student or medical debt?

As an investor, expect thoughtful questions as the advisor gets to know you and observers your visceral reaction to the financial topics. Do you light up when talking about passing your business on to your children? Do you clam up when alluding to student or medical debt?

This is already a pillar of the Stableford Capital culture. The personal relationships we build with our clients give us key insights into their overall attitude and preconceptions about money. This then helps us to positively influence investing and savings habits that will set clients on the right course to meeting their financial goals.

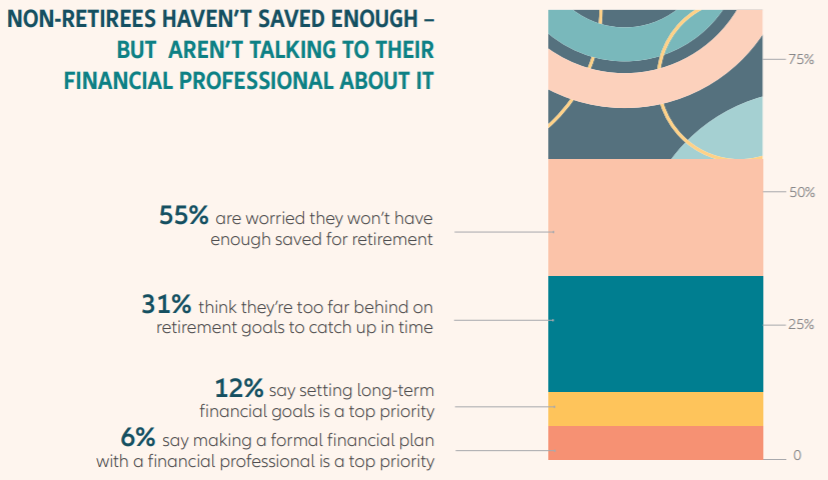

This is particularly true when it comes to retirement savings. Right now, the vast majority of Americans are not “retirement ready.” Practicing behavioral finance can turn the tide and make sure investors continue their financial wellness throughout their retirement.

Building the Basics

Another principle of behavioral finance is fundamental financial education. For most, this starts by watching our parents, then compounds with watching others, media influence, experiences, and advertising. Unfortunately, there’s no guarantee, or evidence, that these sources provide an accurate foundation for finances.

Even when working with a financial advisor, it’s important to understand the basics. This can include the differences between life insurance types, the benefits of owning over renting, and how compound interest works.

Even when working with a financial advisor, it’s important to understand the basics. This can include the differences between life insurance types, the benefits of owning over renting, and how compound interest works.

Without knowing the basics, your preconceptions run rampant. As your advisor, we see it as our responsibility to educate you on the investing process and products, helping you weigh the benefits versus the risks. We leverage our resources and expertise to lead you to financial wellness. We also hold you accountable to turning that education into action.

This behavioral coaching is essential to both client relationships and clients reaching their financial goals.

Breaking Down the 4 Basics: Financial Literacy

Financial wellness is largely about balance, and Behavioral Economist Sarah Newcomb identifies four factors that influence the balance.

As described earlier, many people lack a fundamental financial literacy, both in knowledge and action. This can include how to:

- Pay bills

- Borrow and save responsibly

- Manage money

- Invest

- Plan for retirement

Although financial literacy is important, it’s not enough on its own. The following three factors carry more weight in the balance and financial literacy is strongest when paired with future concept.

Materialism

Those who shop as a hobby, recreation or therapy place a high value on materialism. Feelings are replaced with things. According to both economists and psychologists, we tend to view our possessions as an extension of ourselves, and so what we buy reflects what we feel. However, these feelings are merely temporary. The lost money is permanent.

Impulsiveness

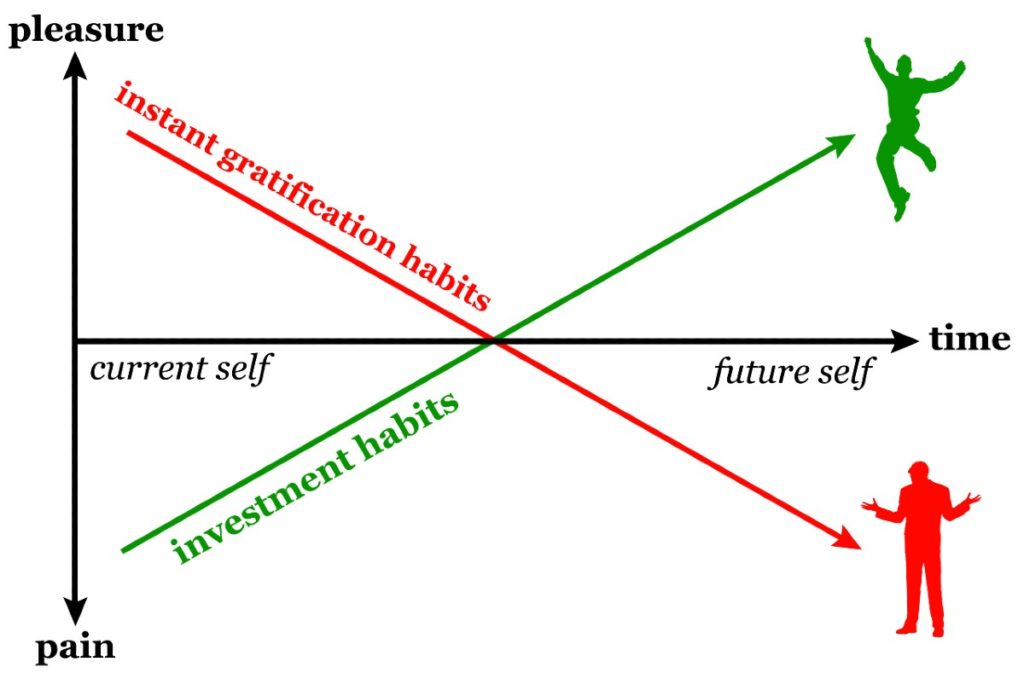

When you don’t have the patience to tolerate “the pain” in waiting to spend, your spending behavior is undisciplined.

To an impulsive spender, the perceived cost of waiting increases the internally calculated cost of the purchase. Thus, an impulsive spender places a higher cost on spending in or saving for the future and is less likely to do so.

To an impulsive spender, the perceived cost of waiting increases the internally calculated cost of the purchase. Thus, an impulsive spender places a higher cost on spending in or saving for the future and is less likely to do so.

Credit card companies take advantage of impulsiveness. When you pay with a credit card, your monthly costs are summed up into one number that can be easily detached from the spending. No emotional attachment to that spending means the pain of waiting to spend is numbed.

And with automatic payments, or digital payments (i.e. smartphone wallets and online stored credit card info), the entire concept of spending goes out the window. The pain-free spending is now brain-free, too.

This is a problem because it is the pain of spending is that actually helps people control their spending. To counteract impulsive spending and focus more on saving for the future, spenders can try tricks like mental imagery and psychological distance.

Future Concept

One way to oppose impulsiveness is through future concept. The future is hard to grasp for many, especially when it comes to finances. Its  much easier to “live in the moment” and reap rewards now than to plan for a future self.

much easier to “live in the moment” and reap rewards now than to plan for a future self.

With future concept, you envision and understand your future self by mentally shortening the distance between right now and the future. Making the future a little more tangible can make it carry more importance, which leads to more rational money decisions.

The power in visualizing your child graduating from college, buying a vacation home or building your business can keep you focused on saving over spending.

The Psychology of Investing = The Psychology of Stress

When it comes to a money mindset, sometimes parental influences are not as strong as environmental ones. Across all generations, and in some cases across the globe, money is the primary cause of stress. And major events in the last two decades have only fueled this, strongly influencing behavioral finance.

After the 2008 financial crisis, many people were nervous to buy real estate again and/or stopped saving for retirement. Now during the COVID-19 pandemic, job security – and in turn financial security – threatens those who were not prepared to absorb temporary financial shocks.

While out of our control, these events do boast the benefit of illustrating a raw look at investors’ current psychology of investing, and thus, how to alter mindsets to be better prepared for a future event.

There will always be future events – behavioral finance helps with the peace of mind to know you can weather the storm and come out stronger.

Financial Wellness – Your Peace of Mind

At its very broad core, the primary purpose of analyzing the psychology of investing and practicing behavioral finance is to get clients to spend less while saving more. This can be challenging and does not happen overnight. Rather, it is the consistent behavioral coaching, series of tweaks to money mindset, and related small changes to money habits that will ultimately be responsible for the transformation to financial wellness and less stress.

At its very broad core, the primary purpose of analyzing the psychology of investing and practicing behavioral finance is to get clients to spend less while saving more. This can be challenging and does not happen overnight. Rather, it is the consistent behavioral coaching, series of tweaks to money mindset, and related small changes to money habits that will ultimately be responsible for the transformation to financial wellness and less stress.

If you’re curious about your own psychology of investing and how it could be affecting your financial wellness, contact Stableford Capital today to schedule a complimentary 15-minute consultation.

excellent piece. I spent 35yrs in the financial services business. your thoughts are spot on! good luck!