Stableford Capital—November 2021 Review: Regime Change

“We’re not even thinking about thinking about raising rates.”

–Jerome Powell, June 10, 2021.

What a difference 5 months makes. On November 30th, Chairman Powell indicated that the Federal Reserve Board would discuss accelerated tapering of asset purchases during the December meeting. The accelerated taper is a clear signal from the Fed: ‘We need to get the taper done faster so we can raise rates and combat inflation.’

The importance of the Fed’s regime change cannot be overstated. Since March of 2020 (and prior), the Fed has made it very clear that rate increases were not an option. Once this was digested by the market in 2020, traders felt emboldened to buy every dip because they knew the Fed would always bail them out by continually inflating asset prices through low rates.

But now, the Fed has signaled that ‘the times, they are a-changin’. Inflation, not growth, is the new top priority (what would you give to have been a fly on the wall in the Biden-Powell re-nomination interview that preceded this change?). The Fed fears that inflation could spiral out of control, so we’ll now hear 100 reasons why jobs can’t structurally get back to the pre-Covid levels in the new Fed messaging. This contrasts with the laundry list of reasons the Fed had been keeping rates low forever.

We happen to agree with many of the reasons to begin the taper (raise rates) and have for a while. In our view, the Fed has been pushing on a string as it tries to increase employment. Of the approximately -4 million jobs difference since January 2020, roughly 1.5 – 2 million were due to early retirement. Many others are a result of lifestyle choices that won’t change soon. The Fed was goosing the economy when there was no benefit. It was simply inflating asset prices (which ironically is one of the biggest causes of inequality in the country—but that’s a discussion for another day) so that those who held real estate, equities, bonds, etc. became wealthier. Eventually, this had to end.

The market is beginning to understand the message. Equities fell 0.8% in November, largely as a result of the Fed’s changed message at the end of the month (Exhibit 1), and have continued their slide in early December.

Equities Drop in November as Fed Regime Change Is Digested

So, what does this regime change really mean? In a word: Risk. At nearly 22x 2022 earnings, equity valuations remain very high by historical standards. The Fed will need to taper/increase rates without spooking the market that it is moving too fast. This is tricky business, akin to pricking a balloon to let the air out slowly without popping it.

Markets know that the cycle has turned. The Fed is going to try to keep the economy going in a Goldilocks scenario (not too hot, not too cold) for as long as possible. But as the equity markets lose confidence that the “Fed has your back”, they could be reluctant to buy dips. Traders will test the Fed’s intentions and quickly discount them through lower prices (to the tune of 5-10%+) if the Fed’s market messaging is off-key.

Moreover, many investors have used derivatives to lock in their gains around the same levels. Should we pierce those levels (around 4500 by most accounts) we could set off a “Gamma trap” where dealers need to continually sell in a downward spiral to avoid losing money. There is no way to know if this will happen, but we can certainly see a heightened risk that this might happen.

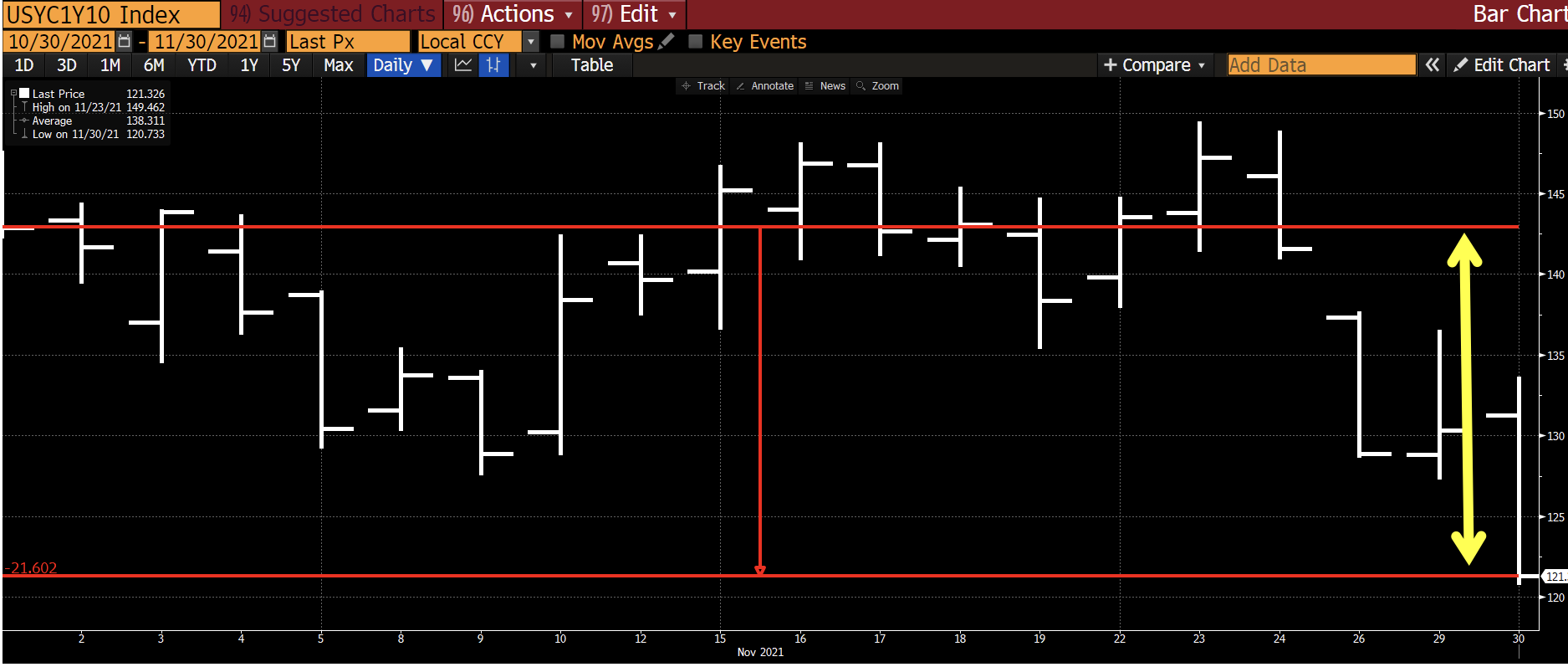

Nominal Rates Drop Slightly in November

Interest rates on the 10 Year US Treasury fell 11 basis points to 1.45% during November. Wait, this doesn’t make sense in an environment when the Fed is raising rates, right? Well, kind of. What happened was treasury curve flattening, when short term rates (which the Fed controls) move up on fears of inflation and Fed taper, while long term rates fall.

This flattening is visible in the spread between 1 Year and 10 Year US Treasury rates. As seen in Exhibit 3, the spread (10-year rates – 1-year rates) fell by 22 basis points during November (and another 12 basis points so far in early December). This occurs because as bond investors anticipate rising rates in the short term (e.g., 1 year out), rates move up over those periods, thus reducing the spread difference. However, another very interesting thing occurs to longer-term rates (e.g., 10-year bonds): Treasury investors begin to worry that the Fed’s moves will choke off future growth. As a result, rates further out on the curve begin to fall as the market anticipates a deceleration in economic activity, further squeezing the spread between 10 year and 1-year bonds.

10 Year – 1 Year Treasury Spread Falls in Anticipation of Higher Short-Term Rates and Slower Future Growth

So, what is Stableford doing: We, like Bob Dylan, recognize when the times are a-changin’ and make what we view as appropriate adjustments. We’ve already started the adjustments and will continue to do so as conditions warrant. As always, we are in tune with the heightened risks, but also remain alert for opportunities to invest more should market conditions over-correct.

Are you interested in making portfolio changes or getting a more in-depth analysis? Contact Stableford today by calling 480.493.2300 or simply request a copy of our Market Blast.

This market commentary was written and produced by Stableford Capital, LLC. Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested in directly. The views stated in this letter are not necessarily the opinion of any other named entity and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

S&P 500 INDEX: The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.