Are 2022 earnings turning negative?

Equites rebounded to close out May unchanged, rebounding from down 5.6% intra-month.

Where are we now?

Thus far in 2022 we have had two parts to the equity downturn. Initially, we had a decrease in valuations, driven by higher interest rates. During May, 10 Year U.S. Treasury yields fell slightly in May to 2.85%, from 2.94%, providing an opportunity for equities to rebound on the hopes of a more dovish Fed.

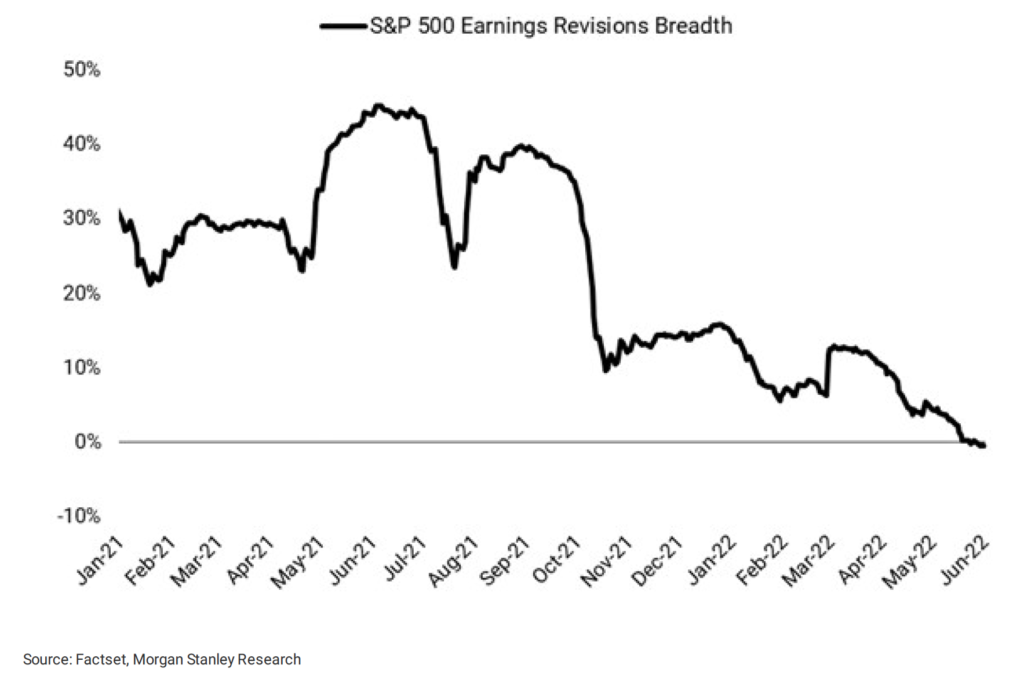

Despite this recent bounce, equities remain in a second phase of the downturn where earnings expectations are starting to come down (as shown by the falling earnings revision breadth in Exhibit 3.) The key from here is whether earnings revisions breadth turns negative and leads to a further correction. While consumers remain strong, companies over-earned during the pandemic. Corporate margins remain high but are at from higher labor and commodity costs. Meanwhile, consumer consumption is moving away from goods toward services (see Target’s double guide-down within 3 weeks).

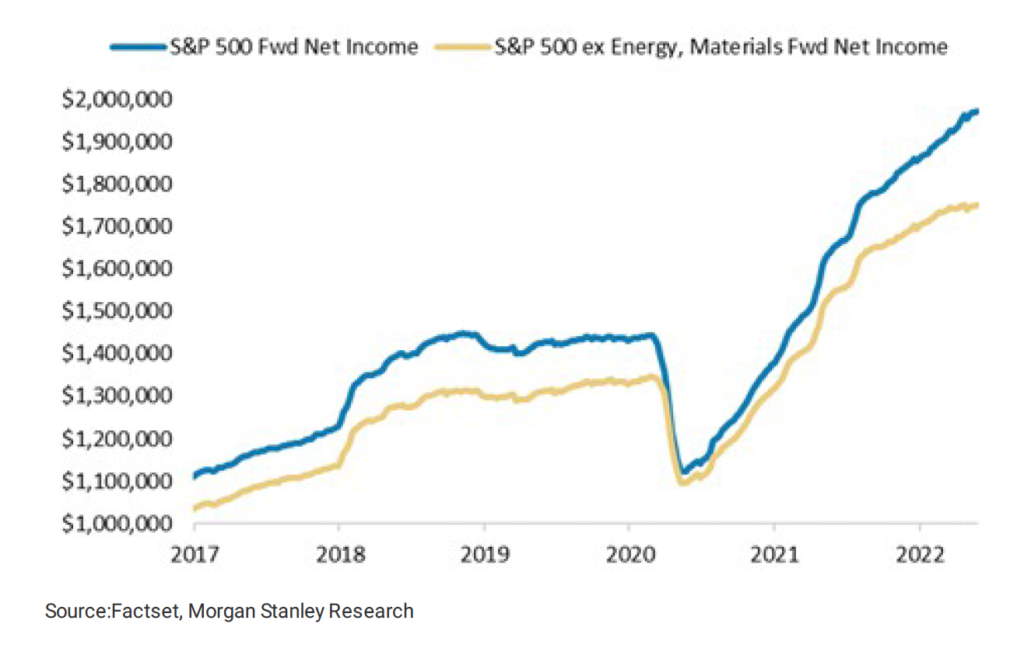

Furthermore, energy and materials are skewing earnings revisions higher, masking some of the weakness. Ex these sectors, earnings are significantly weaker (Exhibit 4). This has already taken its toll in terms of relative performance among sectors year-to-date. We expect it will continue.

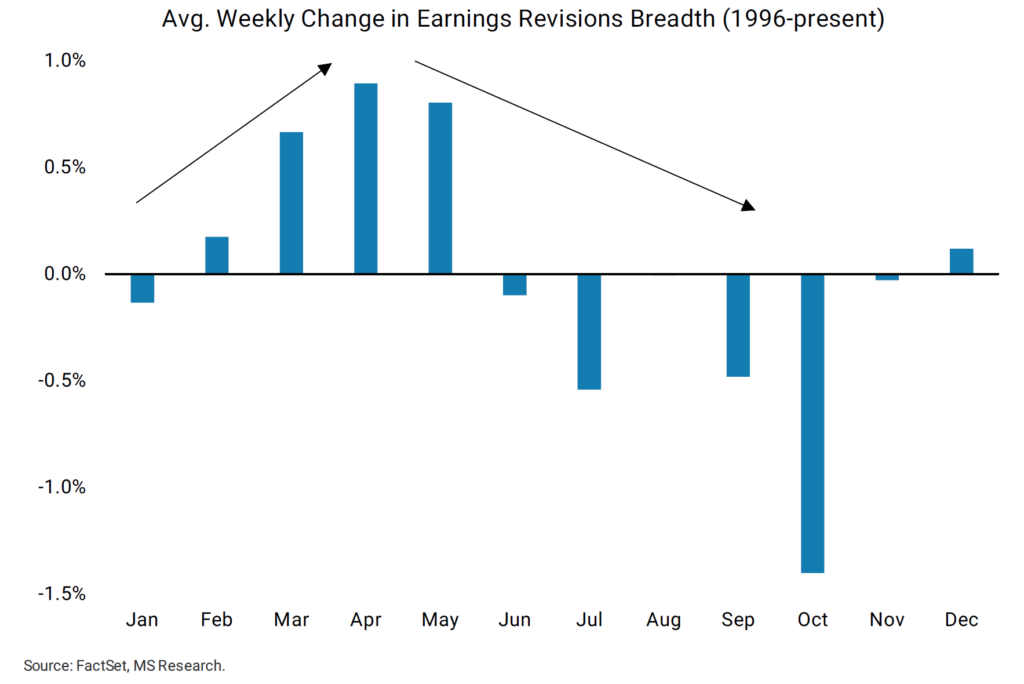

And finally, earnings revisions tend to weaken seasonally after May as companies report 2Q earnings.

Of course, nothing ever moves in a straight line and there are many negatives that could turn positive including China eliminating COVID lockdowns, peace in Ukraine and the Fed slowing its pace of rate hikes. Eventually, all these negatives that are weighing on the market will reverse or be fully priced in. One could argue that most are currently priced in, except the most important one—the Fed—which remains dependent on the pace of inflation.

Please let us know how we may be of assistance in any of your financial planning needs.

Are you interested in making portfolio changes or getting a more in-depth analysis? Contact Stableford today by calling 480.493.2300 or simply request a copy of our Market Blast.

This market commentary was written and produced by Stableford Capital, LLC. Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested in directly. The views stated in this letter are not necessarily the opinion of any other named entity and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

S&P 500 INDEX: The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.