Markets Anticipate Lower Interest Rates

Equities had their biggest monthly mover of 2023 during November as investors anticipated lower interest rates and an economic soft landing.

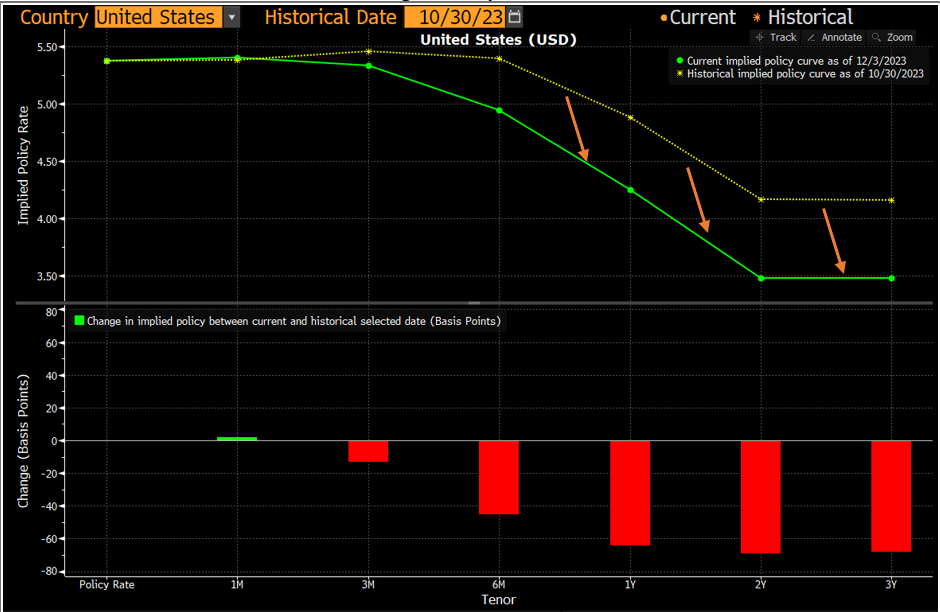

The significant November rebound in equities stands in stark contrast to the disappointing earnings season and 5% rates that drove October lows. The narrative changed markedly in November with weaker economic data and the resulting dovish Fed rhetoric leading investors to anticipate larger interest rate cuts in 2024 from the Fed. The lower yields drove equity valuations up substantially as investors anticipate easier days ahead for earnings. As Exhibit 2 shows, investors now anticipate fed funds to be 60 basis points lower at the end of 2024 than they did a month ago.

As a result, US 10-Year Treasury bond yields also fell a precipitous 60 basis points in November.

So where do we go now? With equities richly priced and expecting an almost perfect soft landing there is little room for error. The key moving forward will be the delicate balance between the slowing economy and fed fund rates. The economy is clearly slowing as the impact of prior rate increases are felt and fiscal stimulus fades. Now the Fed must lower rates fast enough to avoid economic damage but not rekindle inflation. Equities clearly believe the Fed will be successful. But it is crucial that earnings hold up while the economy decelerates.

From our perspective, we believe we’ve seen the highs in interest rates for the cycle. Inflation is slowing, particularly for goods. However, it is very difficult to gauge how quickly the economy will decelerate and where it will level off. What is clear are which sectors are expensive and sporting high expectations. We think that the places to look are early cycle sectors that are still cheap and long-duration fixed income, both of which we’ve been adding to of late.

It is probably best to avoid adding to the more expensive areas of the market such as big cap tech. As we’ve pointed out in the past, equities are a bifurcated market: The equal weight S&P 500 is slightly down on the year (as Exhibit 4 shows), while the S&P 500 (which is weighted by market caps) is up 18%. Nearly all this outperformance can be attributed to the “Magnificent 7” stocks which leads to a narrow and by some measures “risky” market.

Please call with any thoughts or questions

Are you interested in making portfolio changes or getting a more in-depth analysis? Contact Stableford today by calling 480.493.2300 or simply request a copy of our Market Blast.

This market commentary was written and produced by Stableford Capital, LLC. Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested in directly. The views stated in this letter are not necessarily the opinion of any other named entity and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

S&P 500 INDEX: The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.